The Invisible Nature of Digital Transactions

We live in an era where spending saving money has become entirely frictionless and psychologically painless. In the past, when you had to physically open a leather wallet, count out crisp paper bills, and hand them across a counter, your brain experienced a micro-moment of resistance known as the pain of paying.

Today, that resistance has been completely engineered out of society. With a single tap of your smartphone, an automated subscription renewal, or a one-click online checkout, hundreds of dollars vanish from your net worth in a microsecond.

This total lack of friction is why so many hard-working people feel like they are drowning financially despite earning an objective, historically high income. You aren’t necessarily making massive, catastrophic purchases; you are experiencing a slow death by a thousand microscopic cuts. Because digital numbers on a screen do not feel like real, physical resources, it has become remarkably easy to live in a state of continuous financial denial until the monthly credit card statement arrives to slap you back into reality.

The Great Vocabulary Deception

The personal finance industry loves to make money management sound like an incredibly complex branch of advanced astrophysics. They saturate the marketplace with intimidating jargon—like asset allocation, micro-investing platforms, zero-based budgeting models, and algorithmic optimization. They want you to believe that you need an elite background in statistical mathematics just to figure out how to save an extra five hundred dollars a month.

The blunt truth is that money management is roughly ten percent math and ninety percent human psychology. A budget is not an intricate math puzzle; it is simply a physical reflection of your personal values. If you tell yourself that your primary goal is buying a house, but your transaction history shows you spend four hundred dollars a week on upscale restaurants and convenience items, your budget isn’t broken—your priorities are misaligned. True financial health begins the exact second you stop looking for complex mathematical loopholes and start looking honestly at your actual behavioral choices.

The Automated Wealth-Building Blueprint

Step 1: Automated Expense Tracking

The absolute foundation of financial freedom is maintaining an accurate, real-time understanding of where your capital goes every single month. Trying to track this manually is a guaranteed recipe for failure because life simply moves too fast. Modern financial tracking tools revolutionize this process by establishing secure, read-only data pipelines directly with your banking institutions. The second you swipe your card, the transaction is instantly imported, analyzed, and filed away into appropriate buckets.

This automation strips away the emotional weight of logging data and hands you an objective, cold look at your spending behavior. When you see your discretionary categories displayed as an undeniable visual breakdown, the psychological denial vanishes. You can no longer tell yourself that you “don’t know where the money went.” This initial step changes you from a passive passenger into an active director of your personal cash flow.

Step 2: Adaptive Budget Categorization

Traditional budgets fail because they are far too rigid; they expect human life to fit perfectly into neat, static boxes that never change. The moment an unexpected car repair or a friend’s birthday dinner pops up, the entire budget format breaks, the user feels like a total failure, and they abandon the practice entirely. Modern budgeting software fixes this by using flexible, dynamic category limits.

Instead of treating your budget like an unyielding prison sentence, you should treat it like a living, breathing blueprint. If you overspend on groceries during a holiday week, a smart budgeting interface allows you to instantly shift capital from your entertainment or clothing fund to cover the difference. This fluid adaptability removes the toxic guilt associated with overspending and encourages consistent, long-term interaction with your financial goals rather than an endless cycle of restriction and failure.

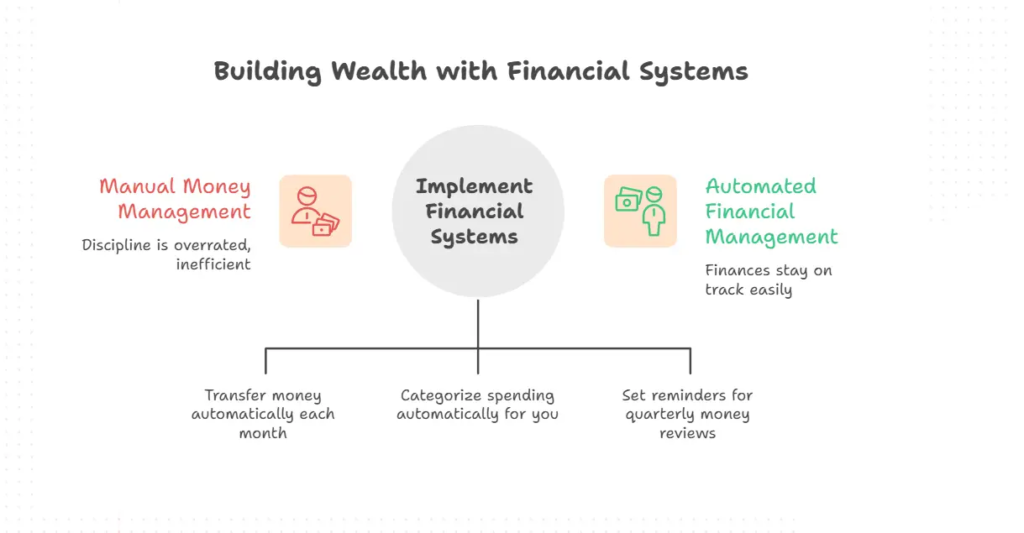

Step 3: The Automated Savings Engine

Relying purely on your own internal willpower to save money at the end of the month is a losing strategy. As long as surplus cash sits lazily in your primary checking account, your brain will subconsciously view it as available spending money, and you will eventually find a way to blow it. To build serious wealth, you must completely remove human decision-making from the equation.

By utilizing automated capital transfers, you can configure your accounts so that a set percentage of your income is instantly swept out of your checking account the exact morning your paycheck lands. This capital should be deposited directly into a designated High-Yield Savings Account or an investment portfolio before you ever have the chance to see it, touch it, or think about spending it. This is the classic rule of paying yourself first, executed with mechanical precision by software that never gets tired or tempted.

Step 4: Visualizing Your Savings Targets

Human beings are fundamentally visual creatures who thrive on feedback loops and visible milestones. Saving money for a vague, distant concept like “the future” feels completely abstract and fails to trigger the dopamine hit our brains crave. Specialized savings goal modules inside financial applications solve this psychological barrier by allowing you to break your total accumulation down into highly specific, visual financial buckets.

Whether you are building a foundational emergency fund, preparing for a home down payment, or funding a vacation, these modules provide interactive progress tracking. Watching a digital progress bar slowly climb from ten percent to ninety percent creates a powerful, addictive sense of tangible accomplishment. It transforms saving from a painful chore of daily self-denial into a highly satisfying, competitive game where you are actively winning against your own past habits.

Exposing Common Financial Distractions

The Allure of the Micro-Investing Mirage

In recent years, the market has been flooded with apps promising to make you wealthy by simply rounding up your daily coffee purchases and investing the spare change into the stock market. While this sounds incredibly appealing on paper, it is largely a marketing gimmick designed to make you feel like you are taking massive financial steps when you are actually standing completely still. Rounding up a three-dollar-and-fifty-cent latte will net you a total investment of fifty cents.

Even over the course of an entire year, those tiny round-ups will rarely total more than a few hundred dollars—an amount that will never move the needle on true financial independence. These apps serve as a dangerous distraction from the real work. If you want to build actual, life-changing wealth, you need to stop playing around with spare change and start making consistent, high-volume monthly investments directly into broad-market index funds.

The High-Yield Myth and Inflation Realities

Another massive point of confusion is the obsession with finding the absolute highest interest rate for a standard savings account. People will spend hours moving money across obscure online banks just to chase an extra fraction of a percent. What they fail to realize is that a savings account is fundamentally a defensive tool designed for capital preservation, not an offensive wealth-building vehicle.

Even the best high-yield savings accounts rarely keep pace with the real rate of core economic inflation. When you factor in taxes on the interest you earn, money sitting in cash is actually slowly losing its purchasing power over long horizons. Your savings account should be reserved strictly for your emergency fund and short-term goals. Any capital intended for long-term growth must be put to work in productive assets like equities or real estate if you want to outrun inflation.

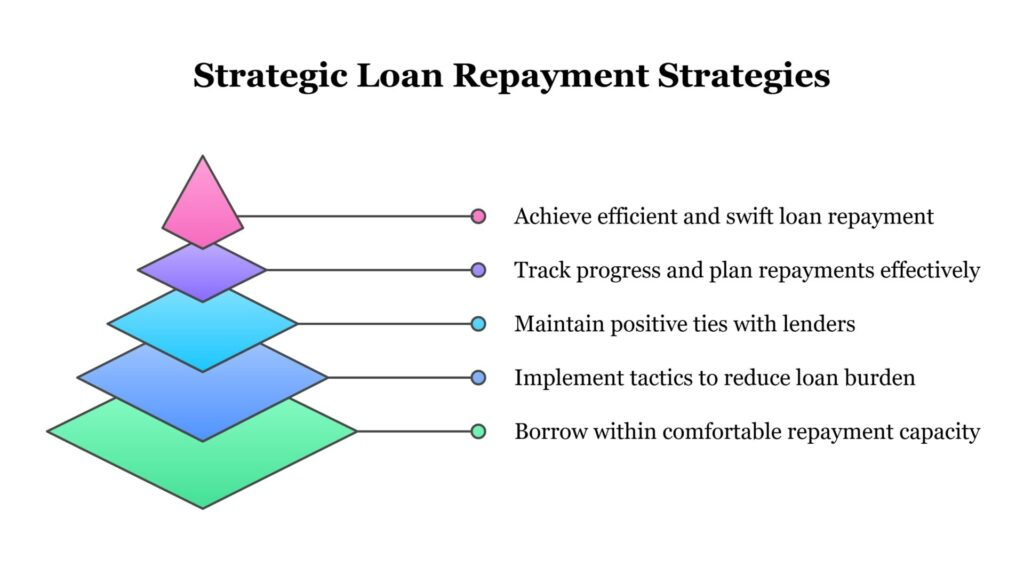

Designing a Bulletproof Repayment Strategy

The Debt Avalanche vs. The Debt Snowball

When it comes to destroying toxic consumer debt, there is an ongoing war between mathematical purity and human psychology. The Debt Avalanche method dictates that you list your debts from the highest interest rate to the lowest and put every extra dollar toward the highest-rate loan first. Mathematically, this is the most efficient strategy because it minimizes the total amount of interest you pay over time.

However, the Debt Snowball method instructs you to wipe out your smallest total balances first, regardless of the interest rate. While less mathematically efficient, the snowball method is often far more successful in the real world because it provides rapid, psychological victories. Eliminating an entire line of debt within thirty days triggers a powerful sense of momentum that keeps you motivated to tackle the larger balances. Modern debt tracking tools allow you to model both scenarios simultaneously, letting you choose the exact balance of math and motivation that fits your personality.

The True Cost of Minimum Payments

The ultimate trap of the modern credit card industry is the deceptively low minimum monthly payment. Credit card companies purposefully design these payments to be as low as humanly possible, often covering just the accrued interest and a tiny fraction of the principal balance. They do this because they want you to stay in debt for decades, transforming you into a reliable, long-term profit center for their shareholders.

If you have a five-thousand-dollar credit card balance at a standard twenty-four percent interest rate and you only make the minimum payment, it will take you over twenty years to pay off that debt, and you will end up paying thousands of dollars in interest alone. Financial tracking tools expose this trap clearly by displaying an explicit interest-cost projection. Seeing the raw, terrifying number of how much money you are throwing away to line a bank’s pockets is often the exact wake-up call required to break the cycle of consumer debt forever.

Stepping Into True Saving Financial Autonomy

Consolidating Your Complete Net Worth

The ultimate goal of using modern financial software is to achieve a single, unified view of your entire financial life—your true net worth. Most people have their lives scattered across five different institutions: a checking account at one bank, an old retirement account with a past employer, a car loan with a finance company, and a mortgage with a separate lender. This fragmentation makes it impossible to see the big picture, leading to a constant, underlying sense of financial anxiety.

By linking all of these disparate accounts into a centralized financial dashboard, you create a singular, undeniable metric of your overall financial progress. Your net worth is simply your total assets minus your total liabilities. Watching this single number grow month over month provides an incredibly grounding sense of security. It shifts your focus away from daily account balances and focuses your attention on long-term wealth building and security.

Embracing the Frictionless Future Resiliently

Technology will continue to advance at a breakneck pace, introducing increasingly powerful tools into our daily lives. We are already seeing the massive rise of AI-powered financial assistants that can predict upcoming utility bills, automatically detect hidden subscription price increases, and recommend optimized tax strategies based on your spending data. These innovations are incredible, but they are ultimately just tools.

The ultimate success or failure of your financial future will always rest squarely on your own willingness to look honestly at your numbers and make intentional choices. Technology can automate the logistics, but it can never supply the personal values or discipline required to build an independent life. Use the tools to strip away the boring, repetitive chores of money management, but maintain active control of the driver’s seat. Your financial freedom is worth the effort.

Frequently Asked Questions

1.What are finance tools?

Finance tools are software applications and digital platforms that help users manage budgets, track expenses, save money, monitor investments, and improve overall financial health.

2.How do budgeting tools help save money?

Budgeting tools track spending, categorize expenses, set spending limits, and provide insights that help users identify areas where they can reduce unnecessary expenses.

3.Are finance tools safe to use?

Most reputable finance tools use advanced encryption and security measures to protect user information. Always choose trusted providers and enable additional security features when available.

4.Can finance tools help reduce debt?

Yes. Many finance tools offer debt tracking, repayment planning, and progress monitoring features that help users pay off debt more efficiently.

5.What is the benefit of automated savings?

Automated savings remove the need for manual transfers and encourage consistent saving habits by automatically moving money into savings accounts.